Jan 2026 – Mar 2026

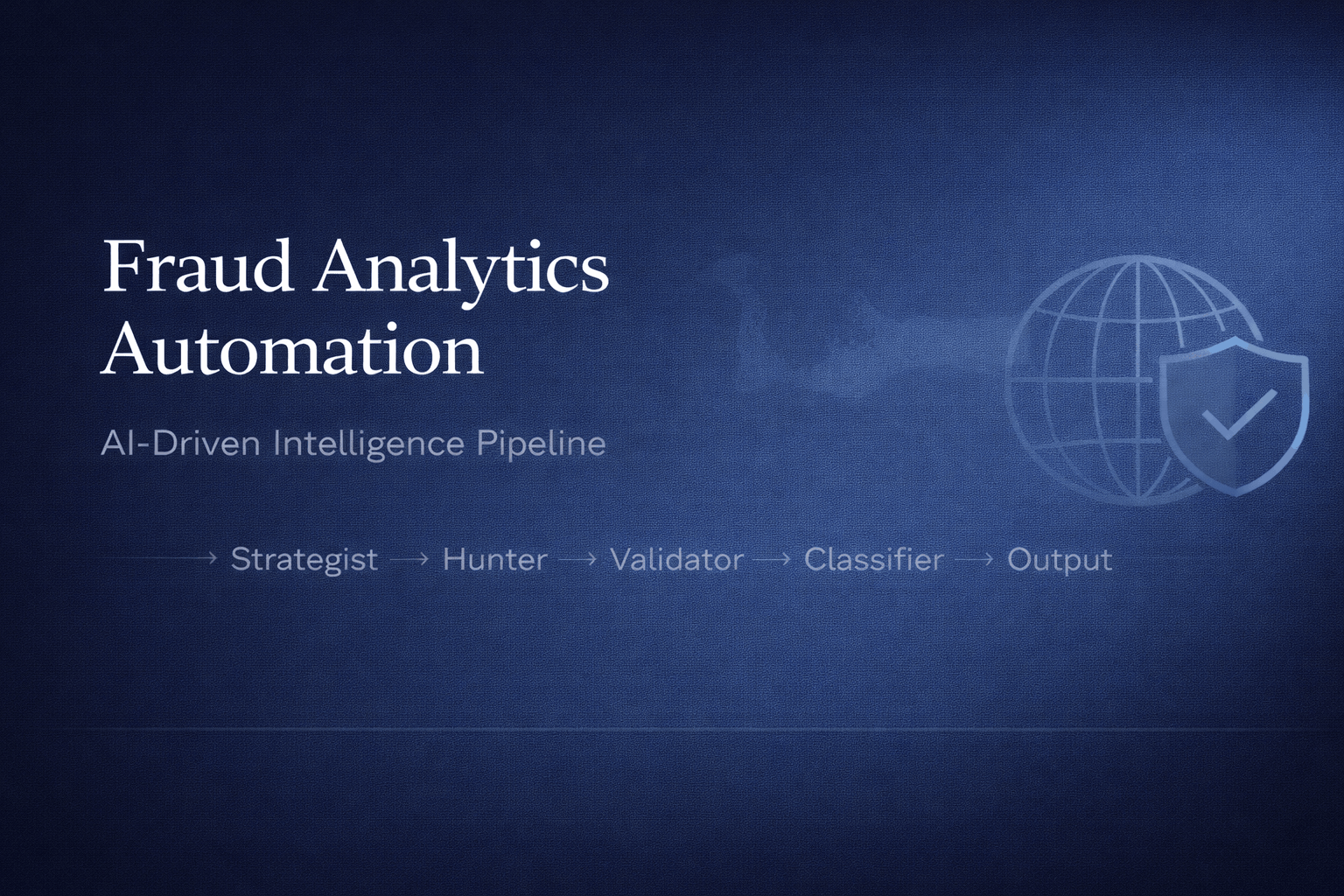

Process Automation

AI-Driven Fraud Intelligence Pipeline

A multi-agent Python pipeline scores emerging fraud risks from unstructured news and runs on Google Cloud Platform.

This project is confidential. A summary report is available on GitHub.